Retrospective and Outlook of M&A in China’s New Energy Industry in 2022

In 2022, the disclosed M&A deal value of China new energy industry M&A amounted to RMB391.7 billion, with a total of 716 deals, hitting a record high level since the start of our reporting. The compound annual growth rate stood at 45% in the past three years, and it is expected to remain high in the future.

Overview of investment and M&A trends

Total deal value

RMB 391.7 billion, up 24%

Total deal volume

716, a 10% increase

Average disclosed deal value

RMB 720million, up 22%

M&A mega deals

3 mega deals exceeding RMB 10 billion, with a total value of nearly RMB 68 billion

Major investment sectors

Lithium batteries, infrastructure, wind power & PV supply chain were the most popular sectors

Active investors

Activities of private enterprises reported a historical high

Main investment direction

Domestic deals, accounts for 95% of both volume and value

Cross-border deals

Outbound deals continue to recover, with deal volume hitting a three-year high

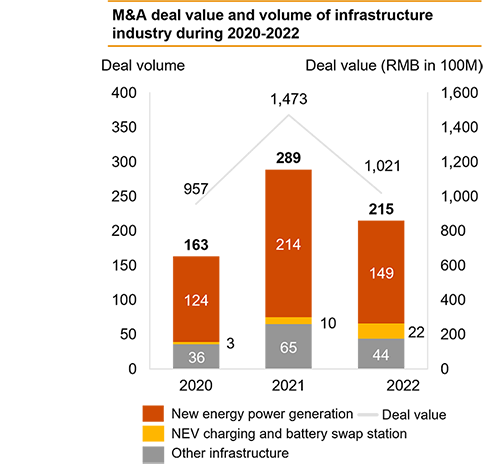

Highlights of M&A deals by sector

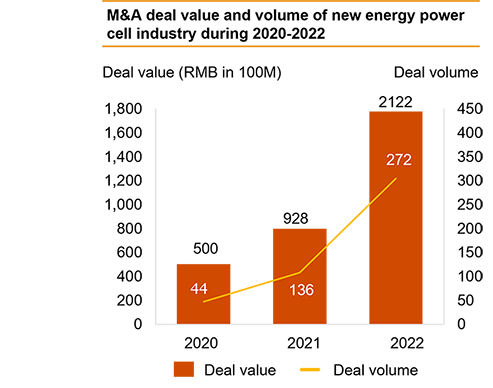

The sectors covers the accelerated development of new energy vehicles that led to the steady increase in investment value of the whole industry value chain including lithium batteries, wind power & PV, energy storage and hydrogen energy, infrastructure sector.

Vertical extension: Battery pack and component firms extend upstream through investment, and form strategic alliances to ensure the supply of raw materials and control costs.

New materials and new technologies: Performance improvement and demand for cost reduction prompt solid-state batteries and silicon-based anode materials to be favoured by investors.

Battery recycling has entered the stage of large-scale investment and has been drawing attention from the market with new energy vehicles gaining increasing popularity.

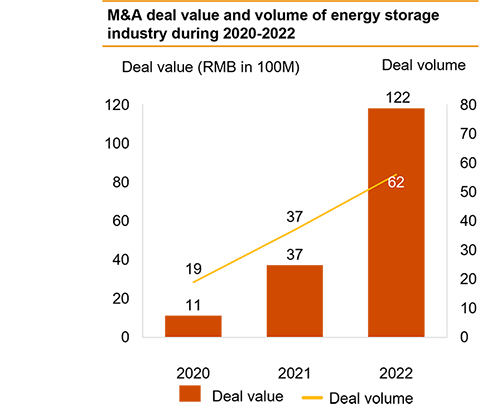

Energy storage integrators highlight advantages of extending both upstream and downstream and are favoured most by investors.

New energy storage technology: The commercialisation of sodium-ion and flow redox batteries speed up to be implemented and the scale of early-stage deals has increased significantly.

Mandatory generation-side energy storage requirements increase the certainty of market size; Consumer-side energy storage has multiple business models and higher profitability; "Dual engine" drives energy storage sector to attract investors.

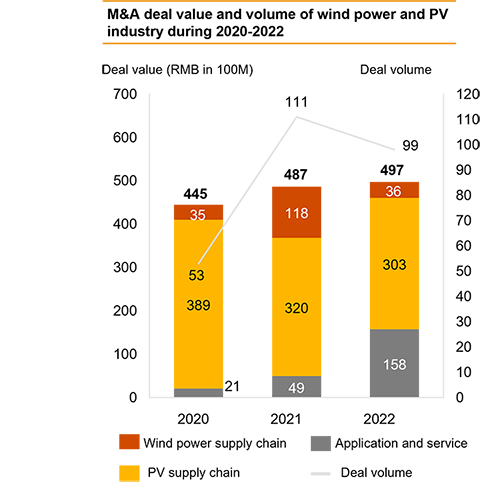

Technology upgrading promotes midstream capability expansion and iteration, while various investors continuously increase investment in different technology routes.

Deepened cost reduction and acceleration in R&D and development of auxiliary components. The willingness to reduce cost and increase efficiency drives industry participants to seek long-term development.

Offshore wind power has emerged as the new battlefield for wind turbines, while product differentiation accelerates the competition of investments in the industry.

Upsizing of equipment drives continuous cost reduction, with turbines and components back into investors' sights.

Year of Compliance for large-scale, centralised power plants; investors tend to be rational and prudent.

The new policies concerning industrial and commercial electricity prices were carried out intensively in various provinces, highlighting the regionalised investments of distributed power plants.

Financial institutions and cross-border investors accelerate rollout, with investors taking on diversified characteristics.

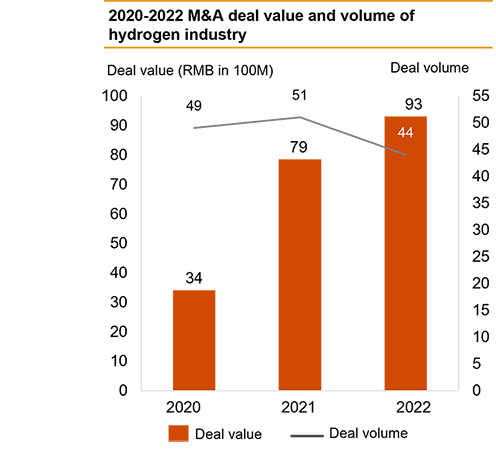

Fuel cell system continues to be the absolute mainstream of the hydrogen energy sector investments and leading enterprises are gradually moving to later financing rounds, with the support of national policies and government as the main driving factor.

The midstream storage, transportation and refilling sector cuts a striking figure, while industrial capital focuses on leading equipment enterprises, while high valued single investments.

The upstream hydrogen production sector has seen a rise, but the financing value and scale are still limited. Leading enterprises have obvious competitive advantages, and the investment and financing activities focus on innovative cutting-edge technologies.

Application scenarios of new energy with hydrogen production are expected to embrace a prosperous future.

Contact us